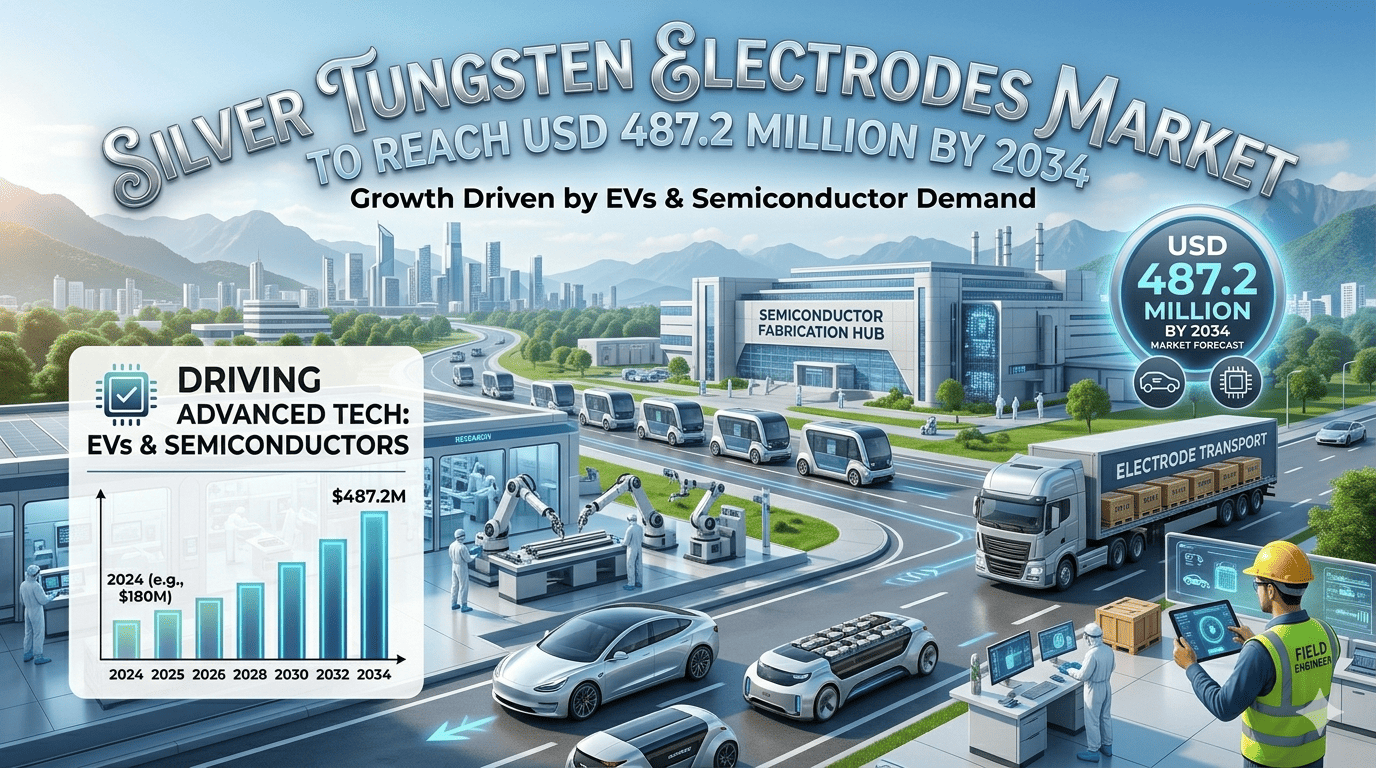

Global Silver Tungsten Electrodes market was valued at USD 342.5 million in 2025 and is projected to reach USD 487.2 million by 2034, exhibiting a steady CAGR of 3.8% throughout the forecast period.

Silver Tungsten electrodes represent a critical class of composite materials engineered to deliver an optimal balance of properties—combining the exceptional electrical and thermal conductivity of silver with the superior hardness, high melting point, and outstanding arc erosion resistance of tungsten. These specialized components are indispensable in high-performance applications such as resistance welding, electrical discharge machining (EDM), and high-voltage switching devices within circuit breakers. Typically composed of 20% to 50% silver by weight, these electrodes ensure reliable operation under extreme thermal and electrical stresses, making them foundational to modern industrial and electronic manufacturing.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307186/silver-tungsten-electrodes-market

Market Dynamics:

The trajectory of the Silver Tungsten Electrodes market is governed by a dynamic interplay of powerful growth drivers, significant adoption restraints, and a landscape rich with opportunity. While the expansion of high-tech industries fuels demand, manufacturers must navigate complex challenges to capitalize on emerging possibilities.

Powerful Market Drivers Propelling Expansion

-

Surging Demand from Electronics and Semiconductor Manufacturing: The relentless advancement and miniaturization within the global electronics sector, a market exceeding $1.5 trillion, creates sustained demand for precision manufacturing tools. Silver Tungsten electrodes are vital for precision welding in micro-component assembly and are crucial in EDM processes for creating intricate molds and dies used in semiconductor production. Their ability to maintain dimensional stability and resist wear during high-precision operations makes them irreplaceable, directly tying their growth to the expanding electronics output, particularly in Asia-Pacific manufacturing hubs.

-

Accelerated Automotive Electrification: The global transition to electric vehicles (EVs) is a paramount growth vector. These electrodes are essential components in high-power relays, contactors, and battery management systems that require materials capable of withstanding frequent high-current switching without degradation. With annual global EV sales projected to surpass 30 million units by 2030, the demand for reliable, durable electrical contact materials is accelerating rapidly, positioning Silver Tungsten alloys as a key enabler of the automotive industry's electric future.

-

Advancements in Material Science and Manufacturing: Ongoing innovations in powder metallurgy and sintering technologies are enhancing the performance and affordability of these composites. Manufacturers are achieving more homogenous microstructures and precise silver distributions, which translate to electrodes with 15-20% longer operational lifespans and improved conductivity. These technological improvements are broadening the application scope, making them viable for more demanding roles in aerospace, defense, and renewable energy infrastructure.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

Significant Market Restraints Challenging Adoption

Despite their superior performance, several barriers can impede widespread market adoption and must be strategically managed.

-

Volatility in Raw Material Costs: The market is highly sensitive to the price fluctuations of its primary constituents, silver and tungsten. Both are globally traded commodities whose prices can swing by 15-25% annually due to factors like mining output, geopolitical tensions, and trade policies. This volatility compresses manufacturer margins and creates pricing unpredictability for end-users, often prompting cost-sensitive industries to explore alternative materials like silver cadmium oxide or copper tungsten, despite potential performance trade-offs.

-

High Initial Investment and Manufacturing Complexity: Producing high-quality Silver Tungsten electrodes is a capital-intensive endeavor. The sophisticated powder metallurgy processes require controlled atmospheres, high-temperature sintering furnaces, and specialized equipment, leading to manufacturing costs that are 20-40% higher than for more conventional contact materials. This high barrier to entry limits the number of new market participants and concentrates production among established specialists, potentially affecting supply chain flexibility.

Critical Market Challenges Requiring Innovation

The journey from laboratory prototype to industrial-scale production presents a distinct set of obstacles that demand continuous innovation and investment.

A primary technical challenge lies in achieving consistent material quality at high volumes. Maintaining a perfectly homogenous mixture of silver and tungsten powders and ensuring uniform sintering is difficult, with batch-to-batch variations still affecting a significant portion of output. Furthermore, technical hurdles in specific applications, such as preventing silver migration in high-temperature DC applications or optimizing porosity for vacuum interrupters, require dedicated R&D efforts. These challenges often consume 10-15% of leading manufacturers' revenues as they strive for product perfection.

Additionally, the market must contend with a complex and sometimes fragmented supply chain. The specialized nature of the raw materials and the logistics of handling metal powders add layers of cost and complexity. Ensuring a stable, high-purity supply of tungsten powder, in particular, is crucial, as impurities can drastically reduce the final product's performance and lifespan.

Vast Market Opportunities on the Horizon

-

Expansion of Renewable Energy Infrastructure: The global push for renewable energy presents a substantial growth frontier. Silver Tungsten electrodes are critical components in the power electronics of solar inverters and the control systems of wind turbines, where reliability under variable loads is non-negotiable. With global investments in solar and wind capacity hitting new records annually, the demand for these high-performance components is set to rise in lockstep with the expansion of clean energy infrastructure worldwide.

-

Development of Next-Generation Alloys: Significant opportunity exists in the R&D of advanced composite materials. Research into nano-engineered alloys and the incorporation of tertiary elements like carbon or nickel aims to create materials with even greater electrical conductivity, enhanced mechanical strength, and superior resistance to arc erosion. Success in these areas could unlock new, high-value applications in next-generation aerospace systems, advanced medical devices, and military hardware, moving the market beyond its traditional industrial base.

-

Strategic Partnerships and Vertical Integration: The market is witnessing a rise in collaborative ventures between electrode manufacturers and end-user companies. These partnerships, focused on co-developing application-specific solutions, are crucial for bridging the gap between material innovation and practical implementation. By working directly with automotive OEMs or electronics giants, manufacturers can tailor their products to exact specifications, reduce time-to-market for new innovations, and secure long-term supply agreements, thereby de-risking investment and fostering stable growth.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented primarily by composition and properties, such as High Conductivity and Low Conductivity grades. High Conductivity electrodes command the dominant market share, prized for their optimal balance of electrical performance and thermal resistance. They are the go-to choice for precision applications like EDM and fine welding where a stable arc and minimal erosion are critical. Low Conductivity variants serve more niche applications where specific resistive properties are required for specialized industrial processes.

By Application:

Key application segments include Resistance Welding, EDM (Electrical Discharge Machining), and Electrical Contacts for switching devices. The EDM segment is demonstrating robust growth, driven by the soaring demand for complex precision tooling and molds from the automotive and consumer electronics industries. While resistance welding remains a foundational application, EDM's growth is fueled by the trend towards miniaturization and complex part geometries that require extremely accurate machining capabilities.

By End-User Industry:

The end-user landscape is diverse, encompassing Electronics & Semiconductor, Automotive, Aerospace, and Industrial Manufacturing. The Electronics & Semiconductor industry accounts for the largest share of demand, leveraging these electrodes in the production of everything from microchips to consumer device components. The Automotive sector is rapidly emerging as a key growth engine, reflecting the industry's massive shift towards electrification and the consequent need for reliable high-power electronics.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

Competitive Landscape:

The global Silver Tungsten Electrodes market is characterized by a semi-consolidated structure with intense competition among specialized manufacturers. The landscape is dominated by firms with deep expertise in powder metallurgy and a strong focus on technological innovation. The top players, including Metal Cutting Corporation (U.S.) and ChinaTungsten Online (China), leverage extensive intellectual property portfolios, advanced production capabilities, and global distribution networks to maintain their positions. Competition is primarily based on product quality, performance consistency, technical support, and the ability to form strategic partnerships with major industrial end-users.

List of Key Silver Tungsten Electrodes Companies Profiled:

-

Metal Cutting Corporation (U.S.)

-

ChinaTungsten Online (Xiamen) (China)

-

AEM Metal (U.S.)

-

Holepop EDM (Japan)

-

MWI, Inc. (U.S.)

-

Mi-Tech Metals (U.S.)

-

T&D Materials Manufacturing (U.S.)

-

American Welding Products (U.S.)

-

American Elements (U.S.)

-

Luoyang Jiangchi Metal Material (China)

-

Stanford Advanced Materials (U.S.)

The overarching competitive strategy revolves around heavy investment in research and development to enhance product performance and reduce manufacturing costs. Alongside internal R&D, forming deep, strategic vertical partnerships with end-user companies is a critical tactic for validating new applications, securing long-term demand, and navigating the complex journey from innovation to commercial success.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: This region stands as the undisputed dominant force in the global market, accounting for over 50% of global consumption. This leadership is fueled by its concentration of electronics manufacturing and semiconductor fabrication giants, particularly in China, South Korea, and Japan. The region benefits from a robust local supply chain, including major producers like ChinaTungsten Online, and strong government support for advanced manufacturing, making it both the largest producer and consumer of these critical components.

-

North America and Europe: Together, these mature markets represent a significant and technologically advanced secondary bloc. North America's demand is driven by its high-tech aerospace, defense, and automotive sectors, which require premium-grade electrodes for critical applications. Europe's market is characterized by strong demand from its precision engineering, automotive, and industrial manufacturing industries, supported by stringent quality standards and a focus on innovative material solutions.

-

South America, and Middle East & Africa: These regions currently represent emerging markets with strong long-term growth potential. Demand is primarily driven by industrialization, infrastructure development, and the gradual expansion of local manufacturing capabilities. While presently smaller in scale, they offer future growth opportunities as their industrial and technological bases continue to develop.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307186/silver-tungsten-electrodes-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307186/silver-tungsten-electrodes-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/