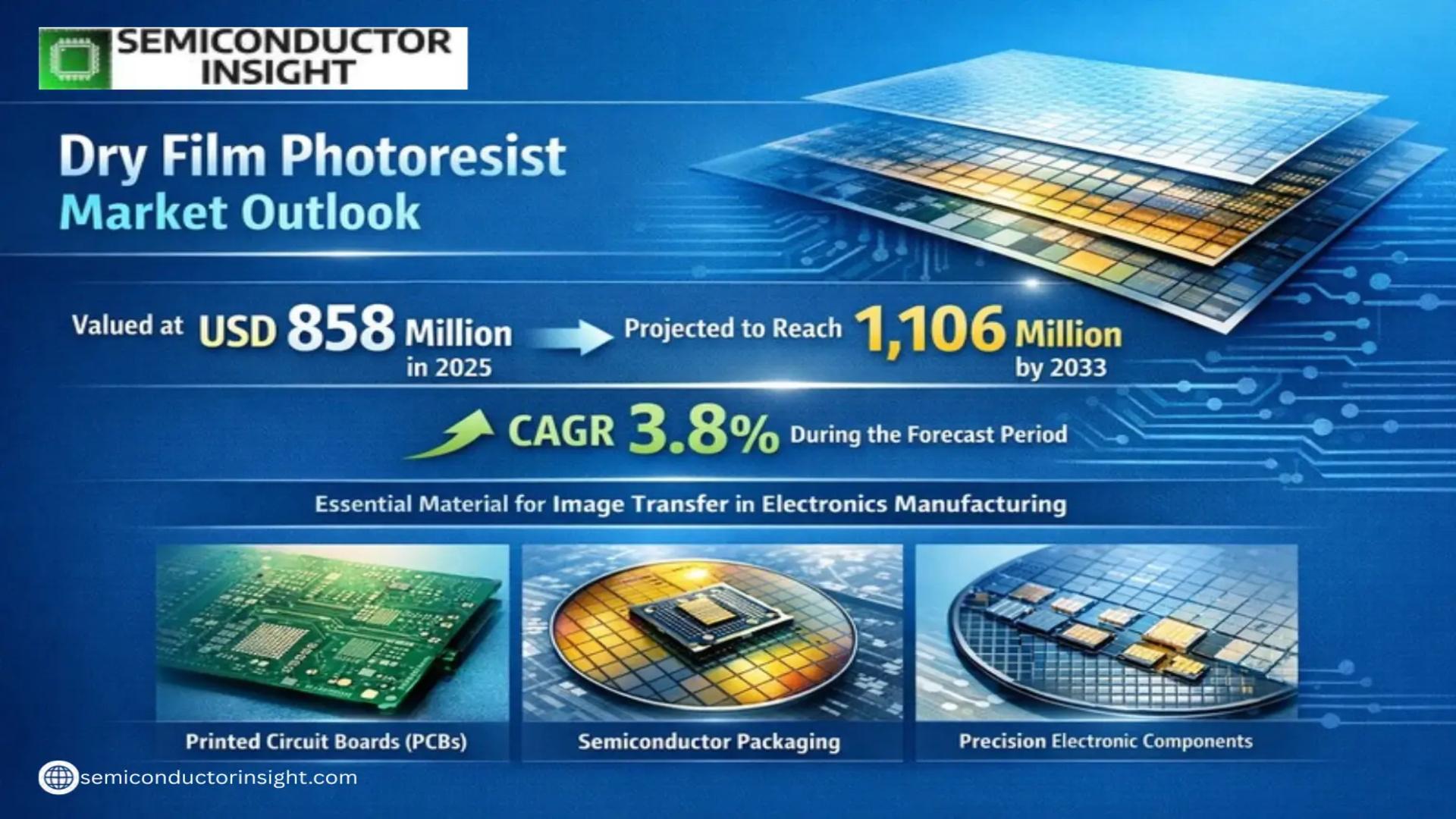

Global Dry Film Photoresist Market was valued at USD 858 million in 2025 and is projected to reach USD 1,106 million by 2034, exhibiting a CAGR of 3.8% during the forecast period 2026–2034. The market reflects steady expansion supported by rising PCB production, semiconductor packaging advancements, and regional manufacturing concentration in Asia-Pacific.

Dry Film Photoresist (DFPR) is a light-sensitive polymer film laminated onto substrates for precision image transfer during the fabrication of printed circuit boards (PCBs), semiconductor packaging substrates, and microelectronic components. Unlike liquid photoresists, DFPR offers uniform thickness control, improved adhesion, and high-resolution patterning capabilities

👉 Access the complete industry analysis and demand forecasts here:

https://semiconductorinsight.com/report/dry-film-photoresist-market/

Market Definition and Dynamics

The Dry Film Photoresist Market operates at the intersection of PCB fabrication and semiconductor packaging innovation. Structural shifts toward electronics miniaturization, IoT device proliferation, and 5G infrastructure deployment are reshaping demand patterns. Asia-Pacific accounts for approximately 73% of global consumption, followed by North America (17%) and Europe (8%), reflecting the geographic concentration of electronics manufacturing capacity.

Market Drivers

- Growing demand for PCBs across consumer electronics, automotive electronics, and industrial systems

- Increasing adoption in advanced semiconductor packaging including FOWLP and 2.5D/3D IC integration

- Miniaturization of electronic components requiring sub-10μm line width precision

- Expansion of 5G infrastructure and IoT devices driving multilayer board fabrication

Market Restraints

- Stringent environmental regulations on photoactive compounds and solvents under REACH and RoHS frameworks

- High material and processing costs compared to liquid photoresist alternatives

- Technical limitations in ultra-fine sub-2μm semiconductor applications

Market Opportunities

- Emerging applications in flexible electronics including foldable displays and wearable devices

- Development of eco-friendly, low-VOC dry film formulations

- Capacity expansion in Southeast Asia aligned with regional electronics supply chain integration

Competitive Landscape

The Dry Film Photoresist Market is consolidated, with Japanese manufacturers maintaining technological and production leadership. Market competition centers on resolution capability, chemical stability, adhesion performance, and environmental compliance. Established players benefit from long validation cycles and strong customer relationships within PCB and semiconductor fabrication ecosystems.

List of Key Dry Film Photoresist Companies

- Asahi Kasei Corporation

- Eternal Materials Co.

- Showa Denko Materials Co., Ltd.

- DuPont de Nemours, Inc.

- Chang Chun Group

- Kolon Industries, Inc.

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Fujifilm Electronics Materials

- JSR Corporation

- Hitachi Chemical Co., Ltd.

- Duksan Hi-Metal Co., Ltd.

- LG Chem Ltd.

- Daxin Materials Corporation

- Guangzhou Guanghua Microelectronics Materials

- Shin-Etsu Chemical Co., Ltd.

Segment Analysis

By Type

- Positive Dry Film Photoresist – Dominates due to superior resolution and compatibility with high-density circuitry

- Negative Dry Film Photoresist – Preferred for applications requiring strong chemical resistance and thermal stability

By Application

- PCB (Printed Circuit Boards) – Largest segment driven by rigid, flexible, and HDI board manufacturing

- Semiconductor Packaging – Rapid growth supported by advanced IC substrate technologies

- Chemical Milling – Utilized for precision metal component fabrication

- Others – Niche microfabrication applications

By End User

- Electronics Manufacturing – Primary consumer across consumer and industrial electronics

- Automotive Industry – Growing integration of advanced PCBs in EVs and ADAS systems

- Aerospace & Defense – Demand for high-reliability circuit fabrication

By Technology

- Subtractive Process – Widely adopted for cost-effective mass production

- Additive Process – Used for specialized circuit formation

- Semi-additive Process – Increasing adoption in fine-pitch applications

By Material Composition

- Acrylic-based – Most widely used due to strong photosensitivity and adhesion

- Rubber-based – Applied in specialized durability-focused environments

- Novolak-based – Utilized for enhanced chemical stability

Regional Insights

Asia-Pacific dominates both production and consumption due to strong semiconductor and PCB ecosystems in China, Japan, South Korea, and Taiwan. Japan accounts for more than half of global production capacity, reinforcing its leadership in chemical engineering and high-performance photoresist innovation. North America maintains demand through advanced semiconductor R&D and defense electronics applications, while Europe emphasizes regulatory compliance and high-end industrial electronics manufacturing.

👉 Access the complete industry analysis and demand forecasts here:

https://semiconductorinsight.com/report/dry-film-photoresist-market/

📄 Download a free sample to explore segment dynamics and competitive positioning:

https://semiconductorinsight.com/download-sample-report/?product_id=127108

About Semiconductor Insight

Semiconductor Insight is a global intelligence platform delivering data-driven market insights, technology analysis, and competitive intelligence across the semiconductor and advanced electronics ecosystem. Our reports support OEMs, investors, policymakers, and industry leaders in identifying high-growth markets and strategic opportunities shaping the future of electronics.

🌐 https://semiconductorinsight.com

🔗 LinkedIn: Follow Us

📞 International Support: +91 8087 99 2013