Global Refrigerated and Frozen Dough Products Market Outlook

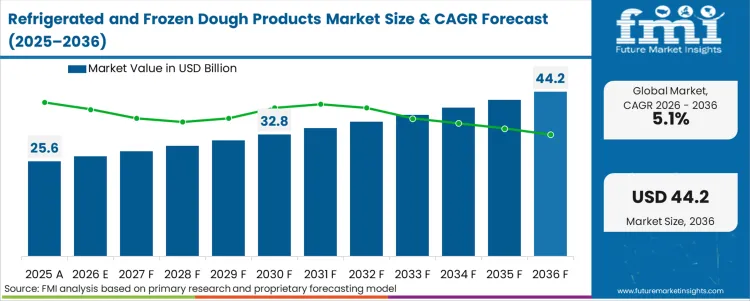

The global Refrigerated and Frozen Dough Products Market has surpassed USD 25.6 billion in 2025, underscoring steady global adoption of ready-to-bake formats across commercial and retail baking ecosystems. According to a new study by Future Market Insights, demand is projected to reach USD 26.9 billion in 2026 and expand to USD 44.2 billion by 2036, reflecting a compound annual growth rate (CAGR) of 5.1% over the forecast period.

This translates into an absolute dollar opportunity of USD 17.3 billion between 2026 and 2036, signaling structural transformation across industrial baking, cold-chain logistics, and retail bakery operations worldwide.

Industrial Baking Shifts from Skill-Dependent to System-Driven Models

Persistent labor shortages across foodservice and wholesale bakeries are accelerating the shift from scratch preparation toward standardized, temperature-controlled dough systems. Pre-portioned refrigerated and frozen dough formats are increasingly positioned as operational risk-mitigation tools rather than optional convenience products.

Simultaneously, global wheat utilization, projected at nearly 794 million tonnes for 2024/25, continues to expose bakeries to protein variability and flour quality volatility. In response, manufacturers are integrating advanced dough-conditioning systems that stabilize water absorption, gas retention, and machinability across high-speed production lines.

Cold-storage constraints are also tightening. As regional freezer capacity utilization increases, processors are relying more heavily on third-party logistics providers to maintain buffer inventories and protect distribution continuity.

Market Snapshot and Key Metrics

- Market Size (2026): USD 26.9 Billion

- Projected Value (2036): USD 44.2 Billion

- CAGR (2026–2036): 5.1%

- Absolute Dollar Growth: USD 17.3 Billion

The sector includes temperature-controlled, pre-mixed, unbaked dough bases used across commercial baking lines and retail freezer aisles. Fully baked ambient pastries and generic industrial flour for non-bakery applications are excluded from valuation.

Segmental Insights: Cookies Lead, Supermarkets Dominate

By type, Cookies and Brownies formats account for 25.8% of global volume share in 2026. Larger, indulgent bakery-style cookies are driving retail innovation. In May 2025, General Mills introduced Pillsbury BIG COOKIES to capture premium at-home baking demand, reinforcing momentum within frozen cookie dough formats.

By application, Supermarkets and Hypermarkets represent 48.2% of total demand in 2026. In-store bakeries increasingly depend on freezer-to-oven systems to reduce waste, standardize output, and meet strict shelf-life mandates.

Operational priorities shaping segment growth include:

- Yield stabilization: Standardized blends offset flour variability and prevent line stoppages.

- Shelf-life extension: Advanced maltogenic amylases delay starch retrogradation, reducing retail shrink.

- Clean-label reformulation: Replacement of mono- and diglycerides with protein-based functional systems enables premium shelf placement.

👉 Get Access to the Report Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-702

Regional Performance: Asia Leads Growth Trajectory

Growth momentum varies across geographies, reflecting differences in industrial maturity and cold-chain infrastructure.

- China: 6.9% CAGR (2026–2036)

- India: 6.4% CAGR

- Germany: 5.9% CAGR

- France: 5.4% CAGR

- United Kingdom: 4.8% CAGR

- United States: 4.3% CAGR

- Brazil: 3.8% CAGR

China leads adoption velocity due to rapid factory automation and retail franchise expansion. India’s expansion is anchored in organized commercial baking transitions supported by growing cold-chain capacity.

In North America, large distribution networks and retailer-driven clean-label mandates are accelerating reformulation initiatives. The United States alone is projected to expand at 4.3% CAGR, supported by extensive refrigerated warehouse capacity and waste-reduction mandates.

European markets, particularly Germany and France, are driven by regulatory scrutiny and clean-label compliance requirements. Manufacturers are deploying advanced biological catalysts to replicate artisanal textures under automated conditions.

In Latin America, Brazil’s reliance on imported wheat continues to elevate demand for enzymatic correction systems that standardize flour functionality and protect margins.

Competitive Landscape: Consolidation Reshapes Technical Capabilities

Strategic consolidation is redefining formulation capabilities and global supply-chain integration. In March 2024, CVC Capital Partners acquired Grupo Monbake to accelerate international expansion. Meanwhile, One Equity Partners announced the acquisition of CraftMark Bakery in 2025 to strengthen ingredient performance capabilities across North America.

Major players shaping competitive dynamics include:

- General Mills

- Grupo Monbake

- CraftMark Bakery

- Europastry

- Art of Baking

- Aryzta

- Rich Products Corporation

- Dawn Food Products

- CSM Bakery Solutions

- Vandemoortele

Scale advantages allow dominant suppliers to co-develop customized protein complexes with multinational baking conglomerates, raising entry barriers and reinforcing long-term contract retention.

Methodology Overview

The analysis is based on a bottom-up modeling framework mapping installed industrial oven capacity against dough inclusion percentages per metric ton of flour. Primary interviews with formulation scientists, procurement heads, and distributors validated commercial utilization rates. Quarterly triangulation integrates supplier earnings disclosures with bulk flour consumption benchmarks.

Frequently Asked Questions (FAQs)

How large is the global market in 2026?

The Refrigerated and Frozen Dough Products Market is estimated at USD 26.9 billion in 2026.

What is the projected valuation by 2036?

The market is forecast to reach USD 44.2 billion by 2036.

What is the growth rate between 2026 and 2036?

The industry is expected to expand at a CAGR of 5.1% over the forecast period.

Which segment leads by type?

Cookies and Brownies formats lead with a 25.8% share in 2026 due to strong anti-staling and premium retail demand.

Which application dominates consumption?

Supermarkets and Hypermarkets account for 48.2% of total demand, driven by in-store bakery efficiency requirements.

Why is China a high-growth market?

Rapid automation, expanding franchise networks, and demand for rheological standardization drive China’s 6.9% CAGR.

What drives demand in North America?

Shelf-life extension, synthetic preservative replacement, and long-haul distribution optimization underpin regional expansion.

What is India’s outlook?

India is projected to grow at 6.4% CAGR, supported by organized industrial baking and expanding cold-chain infrastructure.

Why FMI: https://www.futuremarketinsights.com/why-fmi

Related Reports:

Gluten-free Products Market https://www.futuremarketinsights.com/reports/gluten-free-products-market

Quiet Snacks Market https://www.futuremarketinsights.com/reports/quiet-snacks-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware - 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com