Stainless Steel Market: Building the Backbone of Modern Industry

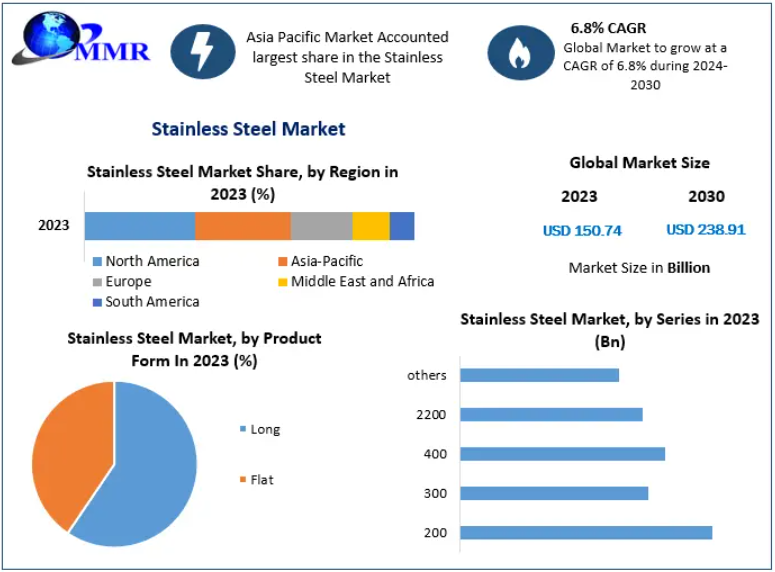

The global Stainless Steel Market continues to play a pivotal role in industrial development, supported by its unmatched strength, corrosion resistance, and versatility. Valued at USD 150.74 billion in 2023, the market is projected to grow at a CAGR of 6.8% from 2024 to 2030, reaching approximately USD 238.91 billion by the end of the forecast period.

Stainless steel’s broad applicability across automotive, construction, energy, consumer goods, and heavy industries positions it as a critical material for both mature and emerging economies. Rising urbanization, infrastructure expansion, and sustainability-driven manufacturing practices are accelerating global demand.

Market Overview

Stainless steel is an alloy primarily composed of iron and a minimum of 10.5% chromium, which forms a passive protective layer that prevents corrosion and staining. Depending on the grade, it may also include elements such as nickel, molybdenum, titanium, and nitrogen, enhancing strength, flexibility, and temperature resistance.

Its durability and hygienic properties make stainless steel indispensable in kitchen appliances, medical instruments, chemical processing equipment, transportation systems, and architectural structures. Manufacturing processes such as melting, hot and cold rolling, and annealing are used to tailor stainless steel for specific performance requirements across industries.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/187313/

Stainless Steel Market Dynamics

Automotive Industry Driving Demand

The automotive sector remains one of the strongest growth engines for the stainless steel market. Manufacturers increasingly favor stainless steel for components such as exhaust systems, fuel tanks, structural reinforcements, bumpers, and decorative trims, owing to its excellent strength-to-weight ratio and corrosion resistance.

The rapid adoption of electric vehicles (EVs) is further boosting demand, as stainless steel is widely used in battery enclosures, thermal management systems, and EV charging infrastructure. Additionally, consumer preferences for premium vehicle aesthetics are driving the use of stainless steel in both interior and exterior automotive designs.

Urbanization and Infrastructure Expansion

Accelerating urbanization is significantly increasing demand for stainless steel in construction and infrastructure development. As cities expand, investments in bridges, tunnels, high-rise buildings, rail networks, and public utilities continue to rise.

Stainless steel’s long lifespan, minimal maintenance requirements, and resistance to harsh environmental conditions make it ideal for large-scale infrastructure projects. According to global urbanization projections, nearly 68% of the world’s population is expected to live in urban areas by 2050, intensifying the need for durable construction materials.

Major landmark projects, including mega-bridges and commercial skyscrapers, have already demonstrated the large-scale consumption of stainless steel, reinforcing its role as a preferred structural material.

Energy and Power Generation Investments

Growing global energy demand is driving investments in power generation and energy infrastructure, creating strong opportunities for stainless steel producers. The material is extensively used in:

- Thermal, nuclear, and hydroelectric power plants

- Wind turbine components

- Oil & gas pipelines and offshore platforms

- Solar panel frames and energy storage systems

Its ability to withstand extreme temperatures, pressure, and corrosive environments makes stainless steel essential for both conventional and renewable energy projects.

Rising Adoption of Recycled Stainless Steel

Sustainability trends are reshaping the stainless steel industry, with recycling emerging as a key growth factor. Stainless steel is 100% recyclable, and most products already contain a significant proportion of recycled material.

Increased recycling helps:

- Reduce dependence on raw materials

- Lower energy consumption

- Minimize carbon emissions

- Improve cost efficiency

Growing environmental awareness and regulatory pressure are encouraging manufacturers to expand recycled content, making stainless steel one of the most sustainable construction and industrial materials available.

Market Restraints

Availability of Alternative Materials

The increasing use of aluminum, advanced composites, and carbon fiber poses a competitive challenge to stainless steel. Aluminum’s lightweight nature and cost advantages have led to its adoption in automotive, aerospace, and construction applications traditionally dominated by stainless steel.

However, stainless steel manufacturers are responding through product innovation, including the development of duplex and precipitation-hardened stainless steels, which offer superior strength and corrosion resistance.

Volatility in Raw Material Prices

Fluctuating prices of key raw materials such as nickel, chromium, and iron ore remain a major challenge. Price volatility impacts production costs, profit margins, and long-term pricing strategies across the stainless steel supply chain.

To mitigate this risk, manufacturers are increasingly investing in vertical integration, recycling technologies, and long-term supply agreements, though raw material volatility continues to influence market stability.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/187313/

Regional Insights

Asia Pacific: Global Market Leader

Asia Pacific dominates the global stainless steel market, supported by rapid industrialization, infrastructure expansion, and strong manufacturing activity. Countries such as China, India, Japan, and South Korea are major producers and consumers of stainless steel.

India’s rising crude steel production and expanding automotive, construction, and energy sectors are contributing significantly to regional growth. Asia Pacific is expected to maintain its leadership position throughout the forecast period.

Europe: Steady Growth Driven by Automotive and Engineering

Europe is projected to experience moderate but stable growth, driven by demand from the automotive, aerospace, and engineering industries. The region’s focus on duplex stainless steel for cost-effective and high-performance applications continues to support market expansion.

Stainless Steel Market Segmentation

By Product Form

- Flat Products (dominant segment)

- Long Products

Cold Rolled Coils (CRC) lead flat products due to strong demand from the automotive sector, while hot rolled bars dominate long products, driven by construction and industrial usage.

By Application

- Automotive & Transportation

- Building & Construction

- Consumer Goods

- Heavy Industries

- Metal Products

- Others

The automotive and transportation segment accounts for the largest revenue share, followed closely by construction and heavy industries.

By Series

- 200 Series

- 300 Series

- 400 Series

- Duplex & Others

By Type

- Austenitic Stainless Steel

- Martensitic Stainless Steel

- Ferritic Stainless Steel

- Precipitation Hard Stainless Steel

- Duplex Stainless Steel

Austenitic stainless steel dominates the market due to its superior corrosion resistance and formability.

Competitive Landscape

The stainless steel market is highly competitive, with companies focusing on capacity expansion, mergers & acquisitions, sustainability initiatives, and advanced product development. Market players are also strengthening global distribution networks and investing in low-carbon steel technologies.

Key Market Players

- Acerinox S.A.

- Aperam Stainless

- POSCO

- Outokumpu

- ArcelorMittal

- Thyssenkrupp Stainless GmbH

- Yieh United Steel Corp

- Nippon Steel Corporation

- Baosteel Group

- Jindal Stainless

Conclusion

The global stainless steel market is set for sustained growth, underpinned by expanding industrial activity, infrastructure investments, energy transition initiatives, and sustainability-driven manufacturing. While challenges such as raw material price volatility and competition from alternative materials persist, continuous innovation and recycling adoption will ensure stainless steel remains a foundational material for modern economies.