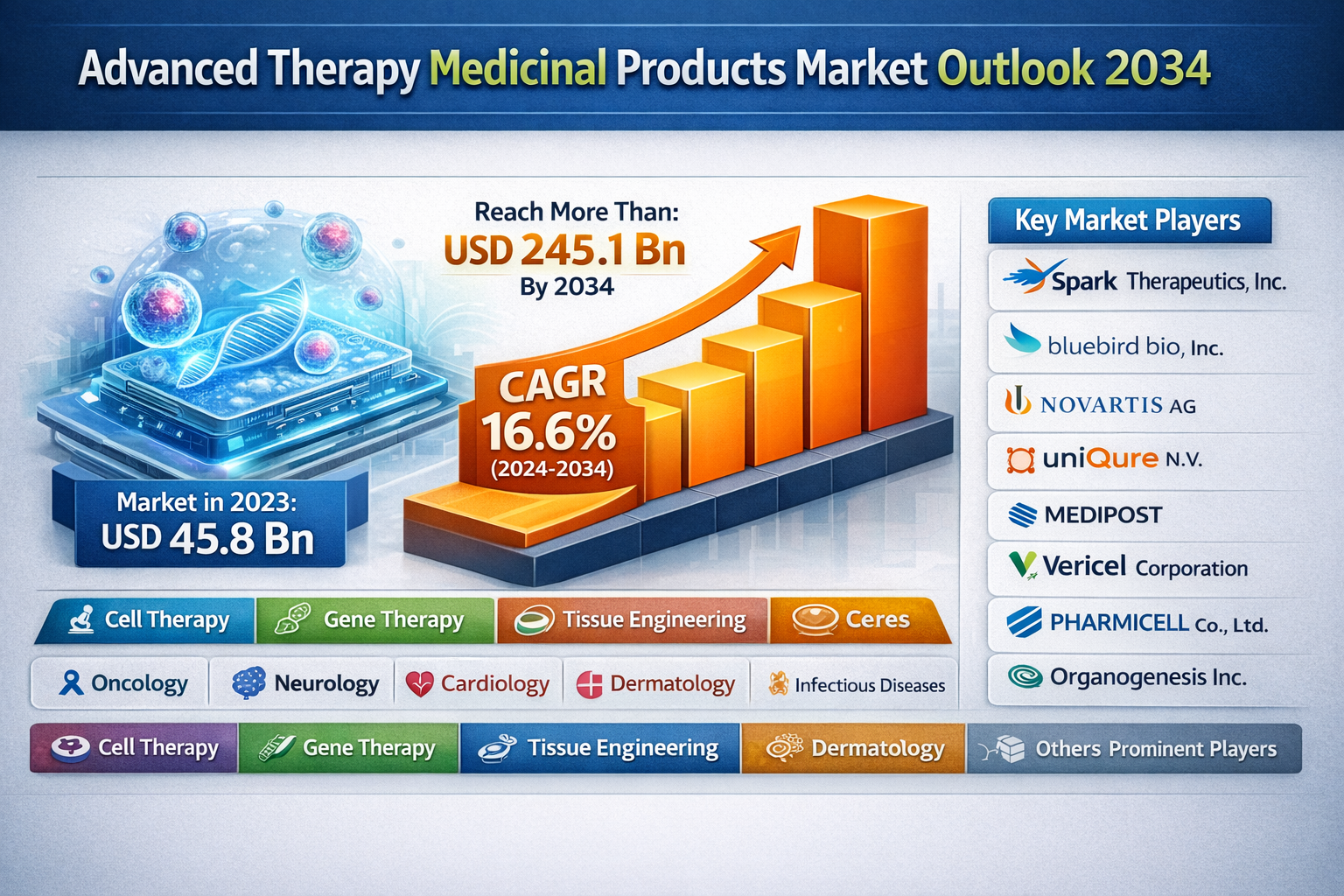

The global Advanced Therapy Medicinal Products (ATMPs) market was valued at USD 45.8 billion in 2023 and is expected to reach more than USD 245.1 billion by the end of 2034. Driven by rapid advancements in gene and cell therapies, increasing approvals of regenerative medicines, and growing investment in personalized healthcare, the market is projected to expand at a robust CAGR of 16.6% from 2024 to 2034, reflecting strong long-term growth potential across key regions.

Surge in demand for tissue engineering, and cell and gene therapy for various indications such as oncology, musculoskeletal disorders, orthopedics, neurology, cardiology, and others is expected to drive the advanced therapy medicinal products market demand.

Transform Your Strategy: Explore In-Depth Data – Sample Available! https://www.transparencymarketresearch.com/checkout.php?rep_id=31298<ype=S

ATMPs include cell, gene, and tissue-engineered, and somatic-cell therapy medicines. They treat the root cause of diseases and disorders by augmenting, repairing, replacing, or regenerating organs, tissues, cells, genes, and metabolic processes in the body.

Market Segmentation

By Service Type

- Manufacturing: Dominates the segment (approx. 45% share) due to the complexity of GMP (Good Manufacturing Practice) requirements.

- Process Development: Crucial for scaling from lab-bench to clinical-grade production.

- Fill-Finish & Packaging: Specialized cryopreservation and cold-chain logistics are vital for living cell products.

- Analytical & Quality Control (QC) Testing: Ensuring safety and potency in highly variable biological materials.

By Sourcing Type

- In-house: Large pharmaceutical companies are increasingly building their own "Factories of the Future."

- Outsourced (CDMO): Small to mid-sized biotech firms heavily rely on Contract Development and Manufacturing Organizations (CDMOs) for specialized infrastructure.

By Application

- Oncology: The largest segment (40-45% share), driven by CAR-T and TCR therapies for hematological and solid tumors.

- Genetic Disorders: Fastest-growing area, focusing on SMA, DMD, and Hemophilia.

- Neurological Disorders: Growing focus on Alzheimer’s and Parkinson’s.

- Cardiovascular & Musculoskeletal: Primarily serviced by tissue-engineered products.

By Industry Vertical

- Pharmaceutical & Biopharmaceutical Companies: Lead in R&D and commercialization.

- Academic & Research Institutes: The primary engine for early-stage discovery and "spin-out" startups.

- Hospitals & Specialized Clinics: The end-users responsible for the complex administration of these therapies to patients.

By Region

- North America: The dominant market (approx. 49% share) due to advanced infrastructure and high healthcare spending.

- Europe: Significant growth driven by centralized EMA regulations and strong academic research bases.

- Asia-Pacific: Projected to be the fastest-growing region (CAGR ~21%), led by China, Japan, and South Korea.

Regional Analysis

North America remains the powerhouse of the ATMP sector, particularly the United States, which benefits from the FDA’s Breakthrough Therapy designations. However, Asia-Pacific is closing the gap, specifically in the cell therapy space. China has become a global leader in the number of CAR-T trials, supported by a massive patient population and significant government backing. Europe maintains a steady hold through its robust regulatory framework for "combined ATMPs" (devices + cells).

Market Drivers and Challenges

Drivers

- Personalized Medicine: Shift toward "N-of-1" treatments tailored to an individual's genetic profile.

- Technological Breakthroughs: Advancements in CRISPR-Cas9, viral vector engineering (AAV, Lentivirus), and 3D bioprinting.

- Chronic Disease Burden: Increasing prevalence of rare genetic diseases and late-stage cancers with no other treatment options.

Challenges

- High Costs: Prices for a single dose (e.g., $2M to $3.5M) create significant reimbursement and accessibility hurdles.

- Manufacturing Complexity: Living drugs are difficult to scale; "the process is the product."

- Supply Chain Logistics: Maintaining the "vein-to-vein" cycle requires ultra-low temperature logistics and rapid turnaround.

Market Trends

- Allogeneic (Off-the-Shelf) Therapies: Moving away from patient-specific (autologous) cells to pre-manufactured batches to reduce costs and wait times.

- AI Integration: Using artificial intelligence to optimize viral vector design and predict patient responses to therapy.

- Non-Viral Delivery: Developing lipid nanoparticles (LNPs) and other non-viral methods to deliver genetic material, reducing the risk of immune reactions.

Future Outlook (2034)

By 2034, the market will likely see a shift from rare "orphan" diseases to more common conditions like heart disease and diabetes through regenerative tissue engineering. Automated "closed-system" manufacturing will become the industry standard, significantly lowering the cost of production and making these therapies accessible to middle-income markets.

Key Market Study Points

- Dominant Therapy: Cell therapy currently holds the largest share, but Gene Therapy is projected to have the highest CAGR.

- Leading Indication: Oncology remains the primary revenue generator.

- Critical Vector: Adeno-associated virus (AAV) is the most utilized vector for in vivo gene delivery.

Competitive Landscape

The market is characterized by a mix of "Big Pharma" giants and specialized biotech innovators. Key players include:

- Novartis AG (Kymriah)

- Gilead Sciences/Kite Pharma (Yescarta)

- Bristol Myers Squibb (Abecma, Breyanzi)

- Bluebird Bio (Zynteglo)

- Spark Therapeutics (Roche)

- CDMO Leaders: Lonza, Catalent, and WuXi Advanced Therapies.

Future Trends:

- In April 2024, Pfizer Inc. announced that the U.S. Food and Drug Administration (FDA) had approved BEQVEZ (fidanacogene elaparvovec-dzkt) for the treatment of adults with moderate to severe hemophilia B who currently use factor IX (FIX) prophylaxis therapy, or have current or historical life-threatening hemorrhage, or have repeated, serious spontaneous bleeding episodes, and do not have neutralizing antibodies to adeno-associated virus serotype Rh74var (AAVRh74var) capsid as detected by an FDA-approved test.

- In January 2024, AbbVie and Umoja Biopharma, an early clinical-stage biotechnology company, announced two exclusive option and license agreements to develop multiple in-situ generated CAR-T cell therapy candidates in oncology using Umoja's proprietary VivoVecTM platform. The first agreement provides AbbVie an exclusive option to license Umoja's CD19 directed in-situ generated CAR-T cell therapy candidates. This includes UB-VV111, Umoja's lead clinical program for hematologic malignancies currently at the IND-enabling phase.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: sales@transparencymarketresearch.com