Food Grade Industrial Gases Market Outlook

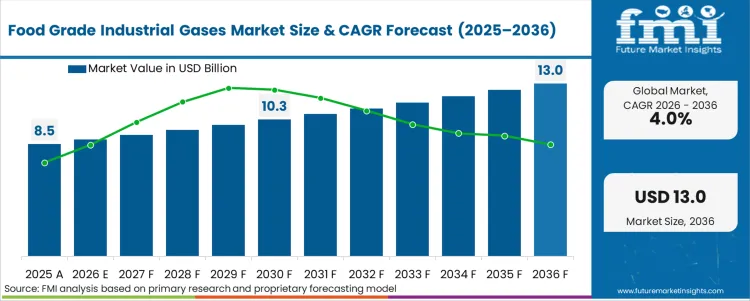

The global Food Grade Industrial Gases Market has surpassed USD 8.5 billion in 2025, underscoring its expanding role in modern food and beverage processing. According to Future Market Insights (FMI), the industry is projected to be valued at USD 8.8 billion in 2026 and reach USD 13.2 billion by 2036, advancing at a steady CAGR of 4.0% during the forecast period.

This growth trajectory reflects the rising structural dependence of beverage bottlers, meat processors, dairy manufacturers, and packaged food companies on purified nitrogen, carbon dioxide, oxygen, and specialty blends for freezing, chilling, blanketing, and carbonation applications.

Food grade industrial gases refer to highly purified atmospheric elements manufactured under strict hygienic conditions for direct use in consumable processing. These gases are essential for preserving freshness, extending shelf life, stabilizing pressure in carbonated drinks, and ensuring microbial safety during packaging.

Despite consistent expansion, supply chain fragility remains a defining operational risk—particularly in beverage and brewery segments. Carbon dioxide shortages linked to upstream ammonia and ethanol plant shutdowns have repeatedly disrupted carbonation-dependent operations. In response, suppliers are restructuring long-term contracts with pass-through pricing clauses to protect margins against volatile energy inputs.

As per Tim Kehoe, Managing Director at Air Liquide Pacific, the company’s partnership with Manildra to develop a biogenic CO₂ solution in Australia demonstrates how supply reliability has become a strategic priority for carbonation-intensive industries.

Market Snapshot (2026–2036 Outlook)

The market’s performance indicators reflect moderate but durable growth:

- Industry Value (2026): USD 8.8 Billion

- Industry Value (2036): USD 13.2 Billion

- CAGR (2026–2036): 4.0%

- Dominant Gas Type (2026): Nitrogen (41.3% share)

- Leading End Use (2026): Beverages (27.9% share)

Nitrogen maintains a commanding position due to its widespread application in modified atmosphere packaging (MAP). Processors inject nitrogen into snack bags, ready-meal trays, and dairy containers to displace oxygen and reduce aerobic bacterial growth. According to the United States Environmental Protection Agency, flexible plastics account for nearly 90% of MAP materials, reinforcing steady nitrogen demand.

Carbon dioxide remains critical for effervescence in soft drinks and beer. However, supply volatility has accelerated internal recovery initiatives. For instance, the Carlsberg Group has invested in CO₂ recovery technology in Sweden, enabling fermentation exhaust capture and reducing merchant supply dependence by up to 40%.

Protein Output and Cryogenic Freezing Sustain Volume Growth

The expansion of global meat output continues to drive demand for liquid nitrogen and carbon dioxide in cryogenic freezing systems. Rapid chilling preserves cellular integrity, locks in moisture, and improves texture retention prior to frozen distribution.

In the United States alone, broiler production reached 61.1 billion pounds in 2024, according to the United States Department of Agriculture. Such production volumes necessitate uninterrupted bulk cryogenic deliveries to maintain operational throughput.

FMI analysts observe a structural shift from mechanical refrigeration toward liquid gas impingement tunnels, creating long-term bulk supply contracts and reinforcing recurring revenue models for merchant gas producers.

Regional Growth Landscape: Asia-Pacific Leads

Demand intensity varies by geography, reflecting protein production volumes, beverage consumption trends, and cold chain maturity.

China is projected to expand at a CAGR of 5.4% through 2036, supported by robust beverage demand and packaged food logistics. Data from the USDA Foreign Agricultural Service indicates that China’s beverage valuation exceeded USD 170 billion, accounting for 12.7% of global intake.

India follows closely with a 5.0% CAGR, fueled by government-backed cold chain expansion. Preservation capacities have exceeded 25.52 lakh metric tonnes, accelerating liquid nitrogen adoption in temperature-controlled warehousing.

In Europe, Germany is forecast to grow at 4.6% CAGR, France at 4.2%, and the United Kingdom at 3.8%, driven by premium packaging requirements and internal carbon capture investments. Strict hygiene enforcement across the region—reinforced by guidance from the World Health Organization—continues to elevate the importance of certified high-purity inputs.

North America remains anchored by protein harvesting intensity, while Brazil’s 3.0% CAGR reflects its role as a dominant meat exporter requiring large-scale cryogenic reserves.

Strategic Imperatives for Industry Participants

To navigate supply volatility and margin pressure, industry leaders are prioritizing:

- On-site nitrogen generation to reduce dependence on merchant bulk distribution networks

- Circular carbon capture systems within brewery and fermentation facilities

- Expanded localized air separation units near high-density agricultural hubs

- Long-term take-or-pay contracts to stabilize procurement costs

Corporate consolidation is also accelerating. In 2025, Air Liquide agreed to acquire DIG Airgas in South Korea for EUR 2.85 billion, strengthening its Asian footprint. Similarly, Messer Group announced a USD 70 million air separation unit investment in Arkansas to expand U.S. capacity.

Competitive Landscape

Major players operating in the Food Grade Industrial Gases Market include:

Linde plc, Air Products and Chemicals, Inc., Messer Group, Taiyo Nippon Sanso Corporation, SOL Group, Coregas, Gulf Cryo, and Iwatani Corporation.

Scale advantages, bundled equipment integration, and plant-as-a-service on-site generation models are increasingly defining competitive differentiation.

👉 Unlock In-Depth Market Intelligence — Access the Full Report Now: https://www.futuremarketinsights.com/reports/food-grade-industrial-gases-market

Frequently Asked Questions (FAQs)

How large is the market in 2026?

The global Food Grade Industrial Gases Market is estimated at USD 8.8 billion in 2026.

What is the projected size by 2036?

The market is forecast to reach USD 13.2 billion by 2036.

Which gas type dominates?

Nitrogen leads with a projected 41.3% share in 2026 due to extensive modified atmosphere packaging utilization.

Which end-use segment drives demand?

Beverages account for 27.9% of total consumption in 2026, primarily driven by carbonation requirements.

Why is Asia-Pacific growing faster?

Rapid urbanization, beverage consumption expansion, and cold chain modernization in China and India are accelerating demand.

What is excluded from the report scope?

Industrial welding gases, medical oxygen, pharmaceutical propellants, and closed-loop refrigerant fluids are excluded.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware - 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com