Executive Summary

The Middle East and Africa Canned Meat Market is undergoing a significant transformation, fueled by rapid urbanization, a burgeoning young population, and an increasing shift toward convenience-driven dietary habits. In a region where climate extremes and logistical challenges often impact the supply of fresh produce, canned meat has emerged as a vital, shelf-stable protein source. The market is characterized by a high demand for Halal-certified products and a growing appetite for premium and organic canned variants in affluent urban centers.

https://www.databridgemarketresearch.com/reports/middle-east-and-africa-canned-meat-market

Market Overview

The Middle East and Africa Canned Meat Market serves as a critical component of the regional food security framework. Canned meat products—including poultry, beef, and seafood—are favored for their long shelf life and ease of storage in arid environments. The market landscape is diverse, ranging from the high-income GCC nations like Saudi Arabia and the UAE, where premiumization and variety drive sales, to African markets where affordability and non-perishability are the primary consumer considerations. The rise of the HoReCa (Hotel, Restaurant, and Cafe) sector and increasing participation of women in the workforce are further accelerating the transition from traditional cooking to ready-to-eat (RTE) solutions.

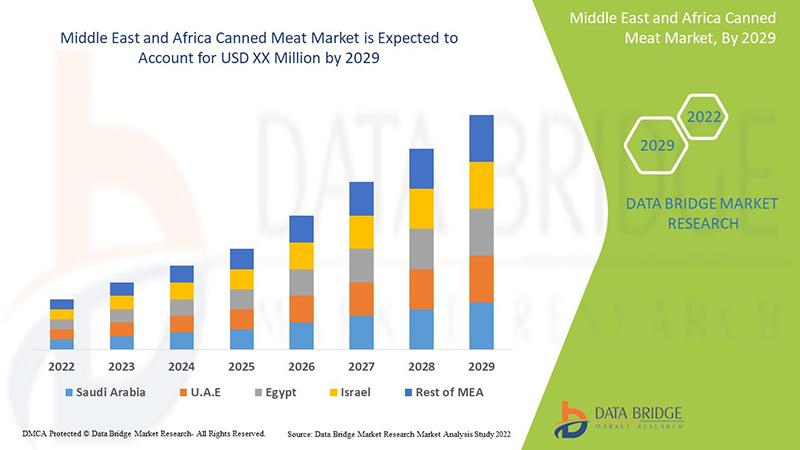

Market Size & Forecast

The Middle East and Africa Canned Meat Market was valued at approximately USD 1.25 Billion in 2024. As infrastructure improves and the retail sector expands, the market is projected to reach USD 1.82 Billion by 2032. This growth is expected to manifest at a Compound Annual Growth Rate (CAGR) of 4.8% during the forecast period of 2025–2032. Saudi Arabia and South Africa remain the dominant revenue generators, while countries like the UAE and Nigeria are identified as high-potential growth pockets.

Market Segmentation

- By Product Type:

- Poultry (Largest segment, dominated by Chicken)

- Beef (Significant share in the Middle East due to Halal demand)

- Seafood (Fastest growing in African coastal regions)

- Lamb and Mutton

- Others (Canned Sausages and Luncheon Meat)

- By Nature:

- Conventional (Dominant share)

- Organic (Rising niche in urban retail centers)

- By Distribution Channel:

- Supermarkets/Hypermarkets: The primary channel for bulk household purchases and brand visibility.

- Convenience Stores: Essential for single-serve and immediate consumption.

- Online Retail: Rapidly expanding, particularly in the GCC, following the post-pandemic digital shift.

- Specialty Stores: Catering to high-end and imported gourmet canned meats.

- By Application:

- Household/Retail

- HoReCa Industry (Institutional use in catering and hospitality)

Regional Insights

The Middle East, led by Saudi Arabia and the UAE, accounts for a substantial portion of the market value. In these nations, high disposable income and a cosmopolitan population drive the demand for a variety of international canned meat brands.

Africa, particularly South Africa and Nigeria, shows robust volume growth. In South Africa, canned meat is a household staple due to its cost-effectiveness compared to fresh red meat. Across the continent, the lack of reliable cold chain infrastructure makes canned meat an indispensable resource for both urban and rural consumers.

Competitive Landscape

The market is highly competitive, featuring a mix of global food giants and strong regional players who specialize in Halal-compliant processing. Key market participants include:

- Americana Group (Kuwait/Saudi Arabia)

- Al Islami Foods (UAE)

- Sunbulah Group (Saudi Arabia)

- JBS S.A.

- Tyson Foods, Inc.

- Hormel Foods Corporation

- RCL Foods (South Africa)

- Zwanenberg Food Group

https://www.databridgemarketresearch.com/reports/middle-east-and-africa-canned-meat-market/companies

Trends & Opportunities

- Halal Certification Excellence: Growing consumer trust in certified Halal canned products is a major driver for regional exports.

- Flavor Fusion: Introduction of regional spices and traditional recipes (e.g., canned Shawarma-style meats) to appeal to local palates.

- Eco-friendly Packaging: A shift toward BPA-free cans and recyclable aluminum packaging to align with global sustainability trends.

- Health-Conscious Variants: Rising demand for low-sodium and preservative-free canned meats in the premium segment.

Challenges & Barriers

- Raw Material Price Volatility: Fluctuations in the cost of livestock and feed directly impact the final retail price of canned products.

- Logistical Bottlenecks: In parts of Africa, inefficient transport networks can increase distribution costs and lead to supply inconsistencies.

- Competition from Fresh/Frozen: In regions with improving cold chain facilities, fresh and frozen alternatives pose a significant threat to the canned segment.

Conclusion

The Middle East and Africa Canned Meat Market is poised for steady growth as it adapts to the modern consumer's need for convenience without compromising on dietary requirements. By focusing on Halal integrity and expanding online distribution, manufacturers can tap into the vast potential of the region's expanding middle class. While economic and logistical hurdles remain, the inherent utility of canned meat ensures its continued relevance in the MEA food basket.

https://www.databridgemarketresearch.com/reports/middle-east-and-africa-canned-meat-market

Browse Trending Report: Middle East and Africa Canned Meat Market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email: corporatesales@databridgemarketresearch.com