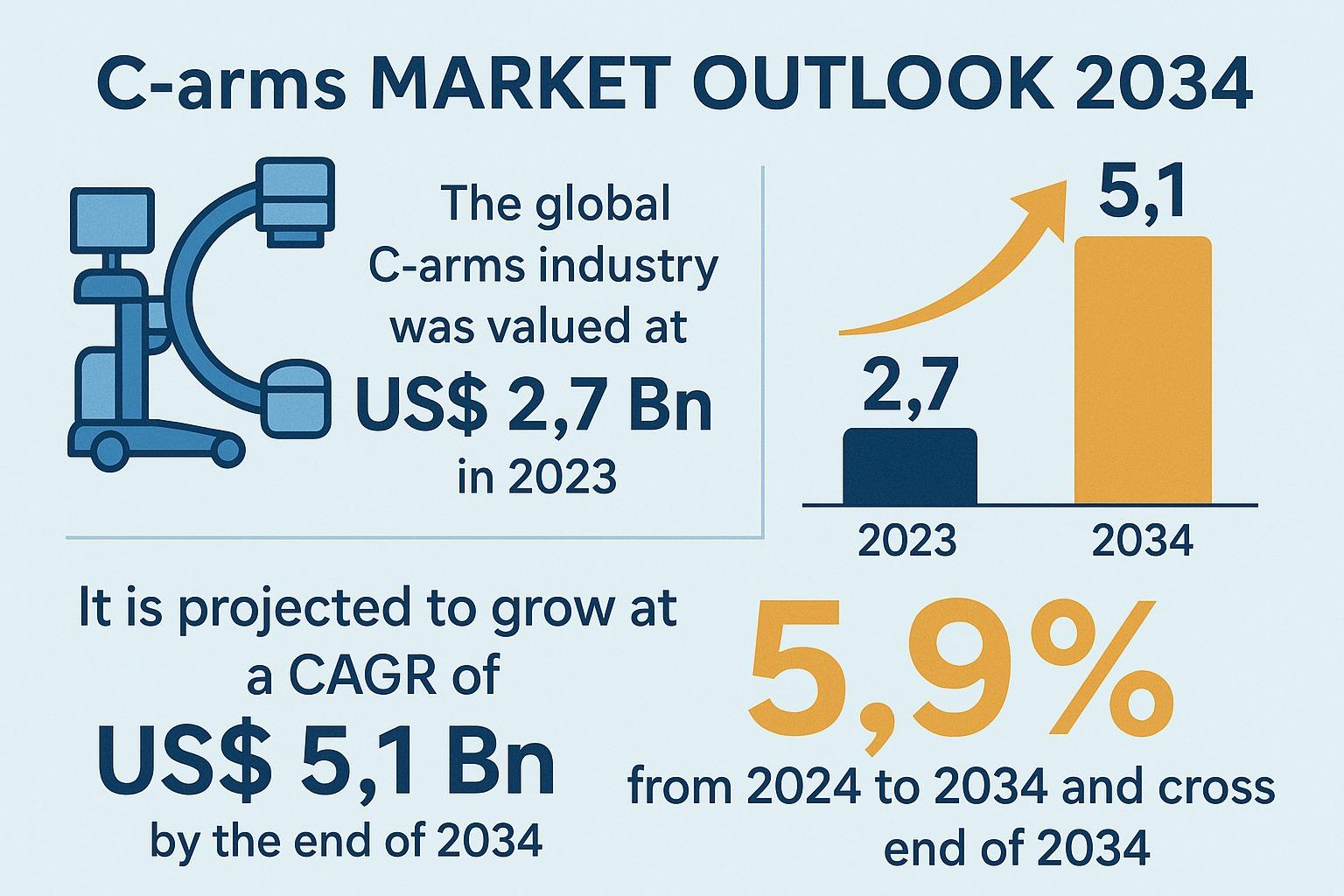

The global C-arms market is entering a decade of notable expansion, underpinned by rapid technological advancements, rising surgical volumes, and the growing prevalence of chronic diseases. Valued at US$ 2.7 Bn in 2023, the market is projected to grow steadily at a CAGR of 5.9% from 2024 to 2034, ultimately surpassing US$ 5.1 Bn by 2034. As healthcare systems worldwide invest heavily in modernization and advanced imaging solutions, C-arm devices have become indispensable tools across multiple clinical disciplines—from orthopedics and cardiology to neurosurgery and gastroenterology.

Analysts’ Viewpoint

According to industry analysts, the C-arms market reflects a dynamic and innovation-driven ecosystem. Growth is significantly propelled by the rising number of minimally invasive surgical procedures, which require real-time, high-quality imaging to improve surgical accuracy. A key factor driving adoption is the expanding geriatric population, which is more susceptible to chronic conditions such as cardiovascular disease, osteoarthritis, and degenerative spine disorders—conditions that frequently necessitate imaging-guided interventions.

Technological upgrades are reshaping market trajectories. Innovations such as digital flat-panel detectors, 3D imaging, AI-powered image enhancement, and radiation reduction technologies are improving image clarity and safety, enabling more accurate clinical decisions. Furthermore, the shift toward mobile C-arms reflects the growing emphasis on flexibility and workflow efficiency in modern operating rooms.

Healthcare infrastructure expansion in emerging markets, especially China and India, presents lucrative opportunities. Increased healthcare spending and a rising preference for high-tech diagnostic equipment are expected to strengthen market penetration in these regions. Overall, C-arm manufacturers are positioned for accelerated growth driven by continuous technological enhancements and expanding clinical applications.

Market Overview

C-arms are advanced fluoroscopy-based imaging devices equipped with a C-shaped arm that connects the X-ray source and detector. They allow clinicians to view anatomical structures in real time, making them essential for surgeries that require continuous imaging guidance. Their role is particularly critical in orthopedic fracture alignment, implant placement, cardiac catheterization, angiography, and numerous minimally invasive procedures.

The demand for C-arms is increasingly tied to the global surge in orthopedic and cardiovascular surgeries. The devices enable precise visualization, reduce operation times, and enhance patient safety. As hospitals prioritize quality outcomes, C-arms continue to gain prominence as essential components of modern surgical care.

Key Market Growth Drivers

High Prevalence of Chronic and Acute Disorders

A significant number of people worldwide suffer from chronic diseases such as cardiovascular disorders, respiratory conditions, gastrointestinal disease, and musculoskeletal ailments. According to the World Health Organization, cardiovascular diseases alone contribute to 17.9 million deaths annually, driving demand for interventional procedures such as angioplasty, angiography, and catheter-based treatments—all requiring C-arm imaging.

Musculoskeletal disorders, fractures, and joint degenerative diseases necessitate surgeries where X-ray–based visualization is crucial. This rising global disease burden directly contributes to sustained C-arms market demand.

Rising Global Geriatric Population

The number of individuals aged 65 and above is projected to reach 2 billion by 2050, constituting 22% of the world’s population. Older adults are highly prone to chronic diseases, fractures, and orthopedic complications such as osteoporosis. Developed countries—including the U.S., U.K., Germany, and Japan—house the largest elderly populations and therefore represent strong markets for high-end imaging equipment.

Improved healthcare access, favorable reimbursement environments, and increasing life expectancy further magnify the need for advanced surgical imaging, strengthening market expansion.

Segment Analysis

Fixed C-arms Lead the Market

Fixed C-arms continue to dominate the market owing to their superior stability, high-resolution imaging, and suitability for complex and lengthy procedures. In orthopedic and cardiac surgeries, fixed C-arms ensure image consistency, enabling precise screw placement, stent positioning, and bone alignment. Hospitals performing high surgical volumes prefer fixed systems for their robustness and long-term reliability.

Orthopedic Surgeries Remain the Largest Application Segment

Orthopedics represents the leading application area due to the global rise in joint replacement surgeries, trauma cases, sports injuries, and spinal disorders. C-arms are crucial for real-time guidance during spinal fusions, vertebroplasty, hip and knee arthroplasty, and fracture fixation. Their ability to minimize surgical errors and optimize implant alignment makes them vital tools for orthopedic surgeons.

Regional Outlook

North America Leads Global Market Share

North America, particularly the United States, is expected to dominate the global C-arms market throughout the forecast period. The region benefits from:

- Advanced healthcare infrastructure

- High adoption of minimally invasive techniques

- Significant surgical volumes

- Favorable reimbursement for imaging technologies

- Strong presence of leading manufacturers

High demand for orthopedic, cardiac, and neurosurgical procedures and rapid integration of next-generation imaging technology further reinforce North America’s leadership position.

Competitive Landscape and Recent Developments

Key players shaping the C-arms market include GE Healthcare, Philips, Siemens Healthineers, Canon Medical Systems, Hologic, Shimadzu, FUJIFILM, DMS Imaging, and Eurocolumbus.

Notable industry developments include:

- March 2024: GE HealthCare showcased advanced solutions in image-guided therapy and CT navigation at SIR 2024, emphasizing innovations in precision care.

- February 2024: Philips launched the Zenition 90 Motorized mobile C-arm featuring enhanced capabilities to support complex vascular and cardiac procedures.

These advancements highlight the industry’s movement toward intelligent, high-precision, and workflow-efficient imaging systems.

Conclusion

The C-arms market is poised for robust growth as surgical volumes rise and hospitals increasingly adopt advanced imaging technologies. With a projected market value exceeding US$ 5.1 Bn by 2034, future opportunities remain strong across both developed and emerging economies. Continuous innovation, growing clinical applications, and increasing demand for minimally invasive procedures will ensure that C-arms remain central to modern surgical and diagnostic practices in the years ahead.