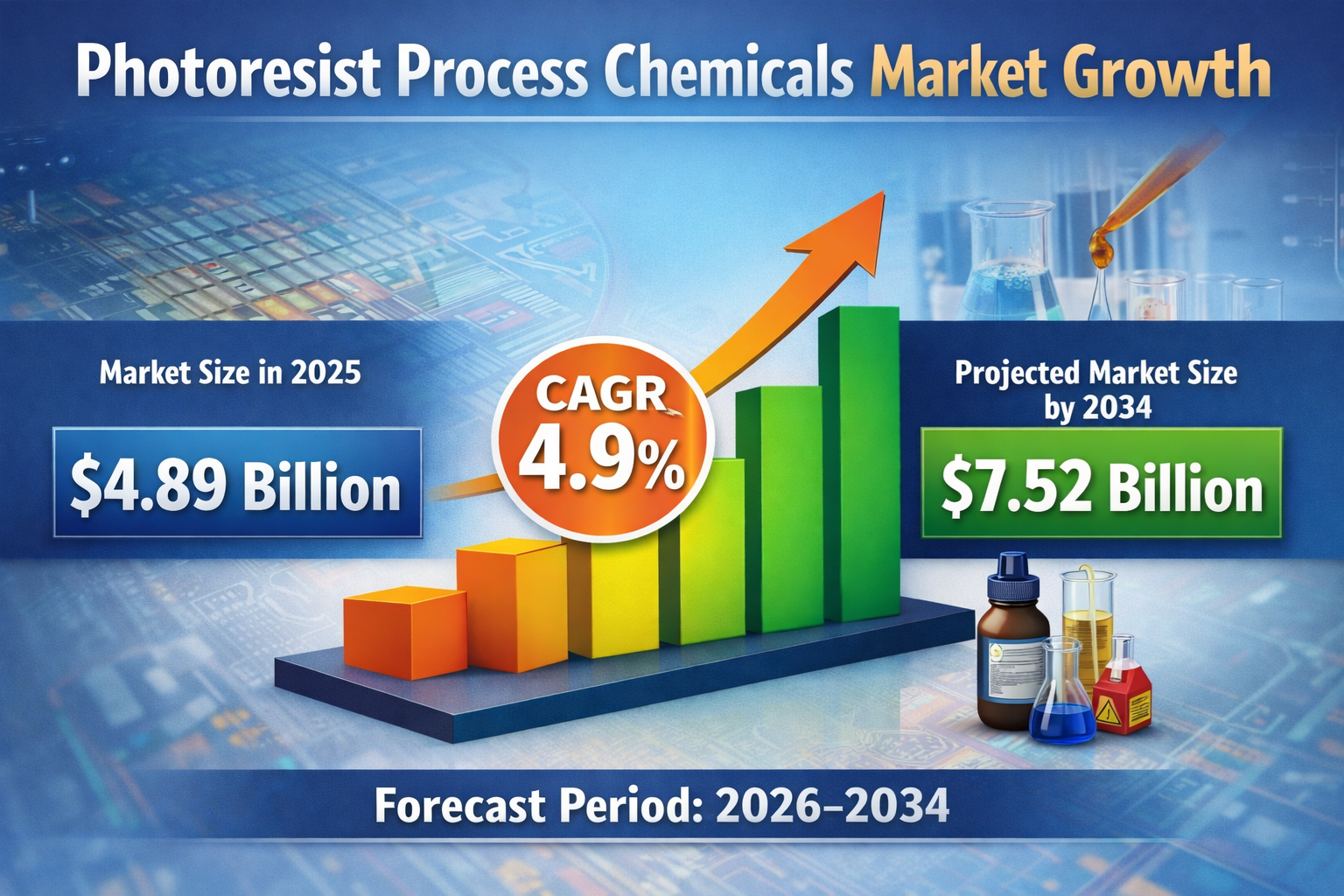

The global Photoresist Process Chemicals Market Report by The Insight Partners covers the period from 2026 to 2034, with historical data spanning 2021 to 2024 and a base year of 2025. The market is projected to grow from US$ 4.89 billion in 2025 to US$ 7.52 billion by 2034, registering a CAGR of 4.9% across the forecast period. The study segments the market by product type solvents, binders, and sensitizer and by application microelectronics and printed circuit boards with geographic coverage across North America, Europe, Asia Pacific, South and Central America, and Middle East and Africa.

Photoresist process chemicals sit at the operational heart of modern semiconductor fabrication, and understanding what drives their demand requires looking past surface-level electronics trends toward the deeper architectural shifts happening inside chip design and manufacturing. The transition toward advanced nodes particularly the widespread adoption of extreme ultraviolet lithography is demanding a fundamentally different chemical performance profile than the processes that defined the industry a decade ago. Purity standards have tightened considerably, and the tolerance window for contamination in sub-seven-nanometer processes is essentially zero.

Request Sample Pages of this Research Study @ https://www.theinsightpartners.com/sample/TIPRE00021610

Market Drivers

The semiconductor industry's relentless push toward miniaturization is the central force shaping demand for photoresist chemicals. Each successive shrink in feature size elevates the performance requirements placed on every chemical in the photolithography stack, from the photosensitive resist itself to the solvents and binders that determine its deposition and removal behavior.

The microelectronics application segment carries the dominant weight of total market demand, and what makes this particularly interesting is the breadth of end-use sectors now feeding into it. Automotive electrification is consuming semiconductors at a pace that would have seemed implausible in previous industry cycles, with advanced driver assistance systems and EV powertrains each requiring dense, highly reliable chips that must meet automotive-grade quality thresholds. This is translating into procurement specifications for photoresist chemicals that go well beyond the conventional consumer electronics supply chain.

IoT proliferation is adding a different dimension to the demand picture not necessarily more advanced chips, but far more of them. The scale implications of billions of connected sensors and edge computing devices means that mid-node semiconductor fabs, which depend heavily on established photoresist chemical platforms, are running at elevated utilization rates with strong forward order books.

Printed circuit board manufacturing is a segment that tends to receive less analytical attention than microelectronics, but the compound growth in high-frequency, high-density interconnect boards for communications infrastructure is generating genuine demand for advanced photoimageable chemistries. Fifth-generation wireless buildout and data center expansion are both consuming PCBs at an accelerating rate, and the board complexity involved in these applications is pulling up the chemical specification requirements across the entire supply chain.

The sensitizer segment occupies a position of particular strategic importance in the current technology landscape. As lithographic wavelengths shrink, the photochemical response of the resist to exposure energy becomes the binding constraint on resolution. Sensitizer chemistry is where much of the current innovation investment is concentrated, and the competitive differentiation between producers in this space is increasingly tied to molecular-level performance rather than production economics.

Competitive Landscape

- Tokyo Ohka Kogyo Co., Ltd.

- Tokuyama Corporation

- DuPont

- Integrated Micro Materials

- Allresist GmbH

- Microchemicals GmbH

- Dischem Inc.

- ENF Technology Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Prolyx Microelectronics Private Limited

Regional Insights

Asia Pacific holds the dominant regional position, driven by the concentration of semiconductor fabrication and PCB manufacturing capacity in China, Japan, South Korea, and Taiwan. North America contributes high-value demand from advanced logic and memory fabs. Europe plays a meaningful role through its specialized automotive-grade semiconductor supply chain.

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as semiconductor and electronics, aerospace and defense, automotive and transportation, biotechnology, healthcare IT, manufacturing and construction, medical device, technology, media, and telecommunications, chemicals and materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In: Korean | German | Japanese | French | Chinese | Italian | Spanish